Understanding the Blockchain Technology for Beginners

Cryptocoins are confusing but if you understand blockchains, you’re halfway home

What is Blockchain Technology?

“The blockchain is an incorruptible digital ledger of economic transactions that can be programmed to record not just financial transactions but virtually everything of value.”

Don & Alex Tapscott, authors Blockchain Revolution (2016)

Blockchain is a technology that allows for fast, secure and transparent peer-to-peer transfer of digital goods including money and intellectual property. In cryptocurrency mining and investing, it’s an important topic to understand.

A distributed database

Picture a spreadsheet that is duplicated thousands of times across a network of computers. Then imagine that this network is designed to regularly update this spreadsheet and you have a basic understanding of the blockchain. Information held on a blockchain exists as a shared — and continually reconciled — database. This is a way of using the network that has obvious benefits. The blockchain database isn’t stored in any single location, meaning the records it keeps are truly public and easily verifiable. No centralized version of this information exists for a hacker to corrupt. Hosted by millions of computers simultaneously, its data is accessible to anyone on the internet.

Blockchain Durability and robustness

Blockchain technology is like the internet in that it has a built-in robustness. By storing blocks of information that are identical across its network, the blockchain cannot:

Be controlled by any single entity.

Has no single point of failure.

Bitcoin was invented in 2008. Since that time, the Bitcoin blockchain has operated without significant disruption. (To date, any of problems associated with Bitcoin have been due to hacking or mismanagement. In other words, these problems come from bad intention and human error, not flaws in the underlying concepts.)

The internet itself has proven to be durable for almost 30 years. It’s a track record that bodes well for blockchain technology as it continues to be developed.

Transparent and incorruptible

The blockchain network lives in a state of consensus, one that automatically checks in with itself every ten minutes. A kind of self-auditing ecosystem of a digital value, the network reconciles every transaction that happens in ten-minute intervals. Each group of these transactions is referred to as a “block”. Two important properties result from this:

Transparency data is embedded within the network as a whole, by definition it is public.

It cannot be corrupted altering any unit of information on the blockchain would mean using a huge amount of computing power to override the entire network.

In theory, this could be possible. In practice, it’s unlikely to happen. Taking control of the system to capture Bitcoins, for instance, would also have the effect of destroying their value.

A network of nodes

A network of so-called computing “nodes” make up the blockchain.

Node - (computer connected to the blockchain network using a client that performs the task of validating and relaying transactions) gets a copy of the blockchain, which gets downloaded automatically upon joining the blockchain network.

Together they create a powerful second-level network, a wholly different vision for how the internet can function.

Every node is an “administrator” of the blockchain, and joins the network voluntarily (in this sense, the network is decentralized). However, each one has an incentive for participating in the network: the chance of winning Bitcoins.

Nodes are said to be “mining” Bitcoin, but the term is something of a misnomer. In fact, each one is competing to win Bitcoins by solving computational puzzles. Bitcoin was the raison d’etre of the blockchain as it was originally conceived. It’s now recognized to be only the first of many potential applications of the technology.

There are an estimated 700+ Bitcoin-like cryptocurrencies (exchangeable value tokens) already available. As well, a range of other potential adaptations of the original blockchain concept are currently active, or in development.

The idea of decentralization

By design, the blockchain is a decentralized technology.

Anything that happens on it is a function of the network as a whole. Some important implications stem from this. By creating a new way to verify transactions aspects of traditional commerce could become unnecessary. Stock market trades become almost simultaneous on the blockchain, for instance — or it could make types of record keeping, like a land registry, fully public. And decentralization is already a reality.

A global network of computers uses blockchain technology to jointly manage the database that records Bitcoin transactions. That is, Bitcoin is managed by its network, and not any one central authority. Decentralization means the network operates on a user-to-user (or peer-to-peer) basis. The forms of mass collaboration this makes possible are just beginning to be investigated.

What Blockchain Is: A general guide

One of the most talked about yet misunderstood topics in recent times, blockchain is completely overhauling the way digital transactions are conducted and could eventually change the way several industries conduct their daily business.

Two words that have rapidly become part of the mainstream vernacular are bitcoin and blockchain, which are often used interchangeably even though they shouldn’t be. While they are related in a sense, these terms refer to two very different things.

Bitcoin is a form of virtual currency, more commonly known as cryptocurrency, which is decentralized and allows users to exchange money without the need for a third-party. All bitcoin transactions are logged and made available in a public ledger, helping ensure their authenticity and preventing fraud. The underlying technology that facilitates these transactions and eliminates the need for an intermediary is the blockchain.

Important: One of blockchain’s main benefits lies in its transparency, as the aforementioned ledger functions as a living, breathing chronicle of all peer-to-peer transactions that occur.

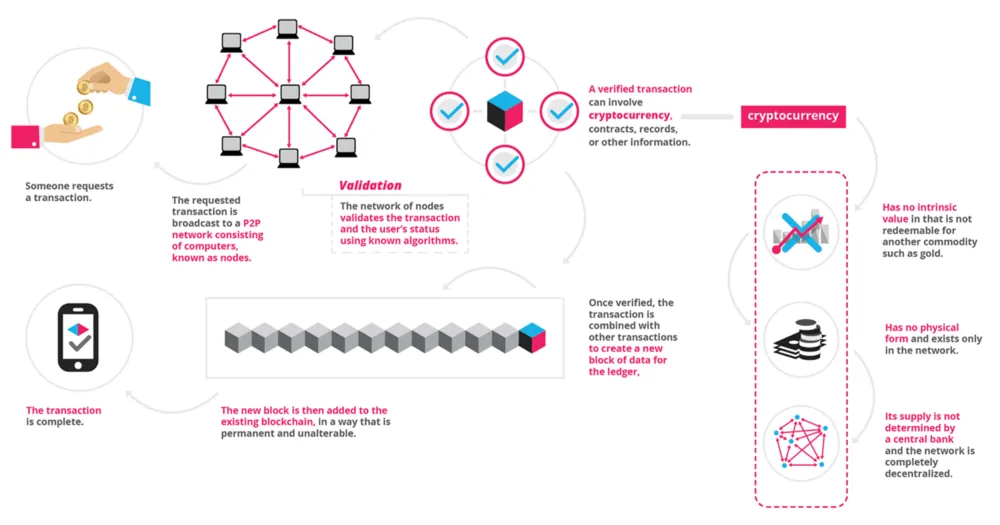

Each time a transaction takes place, such as one party sending bitcoin directly to another, the details of that deal — including its source, destination and date/timestamp — are added to what is referred to as a block.

This block contains the transaction in this example along with other similar types of transactions that have been recently submitted, usually within the past ten minutes or so when you’re dealing with bitcoin in particular. Intervals may vary depending on the specific blockchain and its configuration.

Important: The validity of the transactions within the cryptographically-protected block is then checked and confirmed by the collective computing power of miners within the network in question.

On an individual basis, these miners are computers which are configured to utilize their GPU and/or CPU cycles to solve complex mathematical problems, passing the block’s data through a hashing algorithm until a solution is found. Once solved, the block and all of its respective transactions have been verified as legitimate. Rewards (bitcoin, in this example, but it could be Litecoin or some other currency) are then divvied up among the computer or computers that contributed to the successful hash.

Tip: Now that the transactions within a block are deemed valid it is attached to the most recently verified block in the chain, creating a sequential ledger which is viewable by all who desire.

This process continues in perpetuity, expanding upon the blockchain’s contents and providing a public record that can be trusted. In addition to being constantly updated, the chain and all of its blocks are distributed across the network to a large number of machines.

This ensures that the latest version of this decentralized ledger exists virtually everywhere, making it almost impossible to forge.

Why Blockchain is Needed

Peer-to-peer connectivity over the internet has existed for quite some time in a number of different formats, allowing for the distribution of digital assets directly from one person or business to another.

Since we can already send these bits and bytes to each other, what’s the point of using a blockchain?

The behavior of the Bitcoin blockchain is the perfect example to answer this question. Pretend for a moment that there was no blockchain in place, and that you had one bitcoin token in your possession with its own unique identifier assigned to it.

Now, let’s say you wanted to buy a new television from a business that accepts cryptocurrency, and that shiny new TV happens to cost one bitcoin.

Unfortunately, you also need to pay back your friend for the bitcoin which you borrowed from him last month.

In theory, without the blockchain in place, what’s to stop you from transferring that same digital token to both your buddy and to the electronics store?

This dishonest practice is called double-spending, and it’s one of the main reasons why peer-to-peer digital transactions have never really caught on until now. With blockchain, which not only distributes a public record of all transactions but confirms a block before each of its individual transactions can be finalized, the possibility of this fraudulent activity is essentially wiped out.

While in the past we had no choice but to rely on intermediaries such as banks and payment processors to validate these transactions and make sure that everything was on the up and up, for a nominal fee of course, blockchain technology lets us truly transfer our digital assets from point A to point B taking comfort in the fact that there are reliable checks and balances in place.

Exploring the Blockchain

As we’ve already discussed, the ability for anyone to view a public blockchain such as the one associated with virtual currencies like Bitcoin is a key factor in why it works as well as it does. The easiest way to peruse this distributed database is through a block explorer, typically hosted on a free-to-use website such as Blockchain.info.

Most blockchain explorers are heavily indexed and easily searchable, allowing you to locate transactions in a number of different ways including by IP address, block hash or other relevant data points.

Other Uses for Blockchain

Blockchain has come to the forefront of many discussions because of its role in the distribution of cryptocurrencies like Bitcoin. In the long run, however, these digital cash transactions may end up being a very small part of blockchain technology’s overall footprint on the world as a whole and the way we transfer assets online.

The possibilities for blockchain implementation seem endless, as its underlying technology can be leveraged in virtually any field to perform a number of important tasks such as the following.

Executing contracts

Safely buying and selling intellectual property

Distributing important medical information

Ensuring that voting in elections is incorruptible

We, as a world society, have just begun to scratch the surface here. New potential uses for blockchain are being discovered on a regular basis.

Private blockchains will allow companies to revolutionize their own internal processes while public, open-source variations will continue to change the way we handle business in our daily lives.