I've been exploring DeFi projects these days. Yesterday I was walking through Compound, a decentralized rending service based on its protocol. The Compound token (COMP) led this summer's DeFi hype.

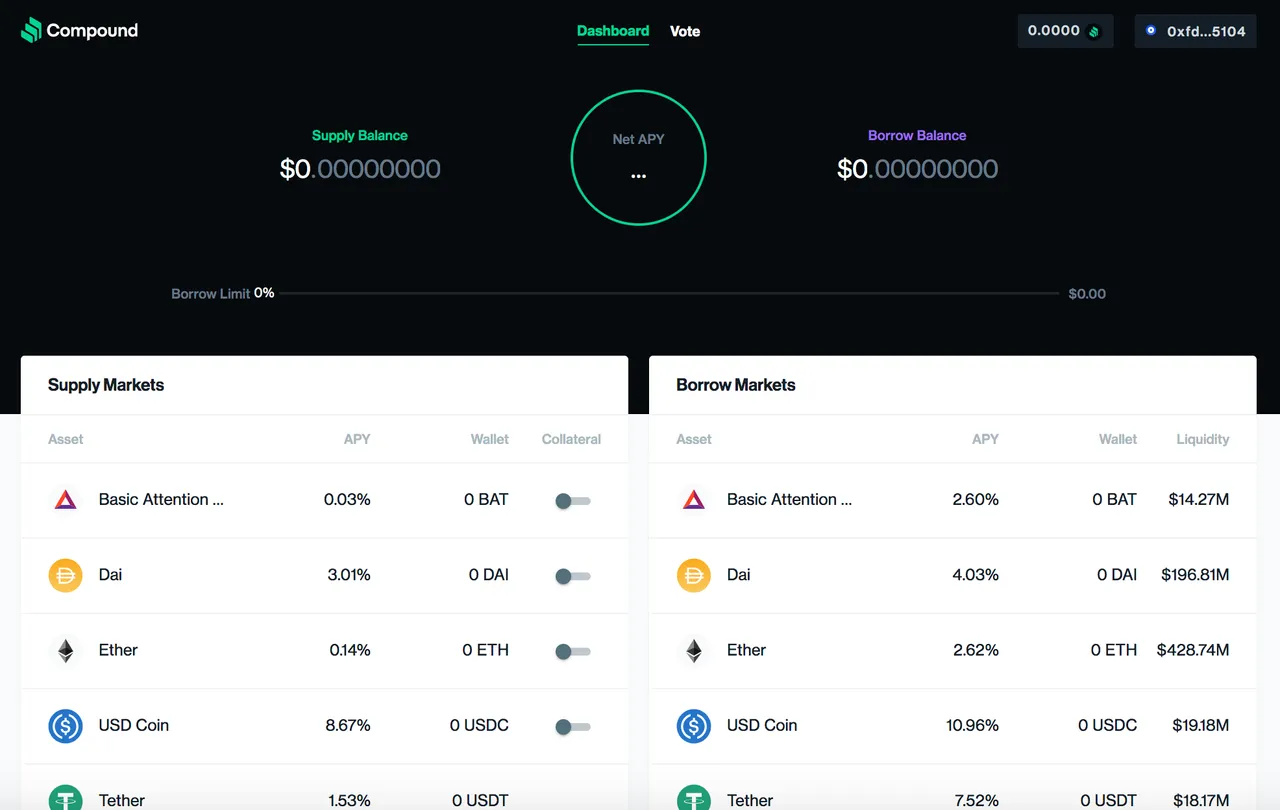

You can connect your wallet and start lending/borrowing cryptos such as Ether, Dai etc. APY(Annual Percentage Yield) is changing over time but some have quite good number. APY is a kind of realtime interest rate. USD Coin and Tether have a good APY while Ether has a low APY. I guess it because people tend to hold more volatile ones as crypto price is bullish these days. I wonder it is vise versa when crypto is bearish. We'll see!

And the APY shown in the list is just one side. Compound token is also distributed to not only lenders but also to borrowers.

I use N26, a mobile bank in Germany. The best interest rate for saving accounts is 1.57%. I even don't know or care my other bank, Volksbank, a conventional German bank.

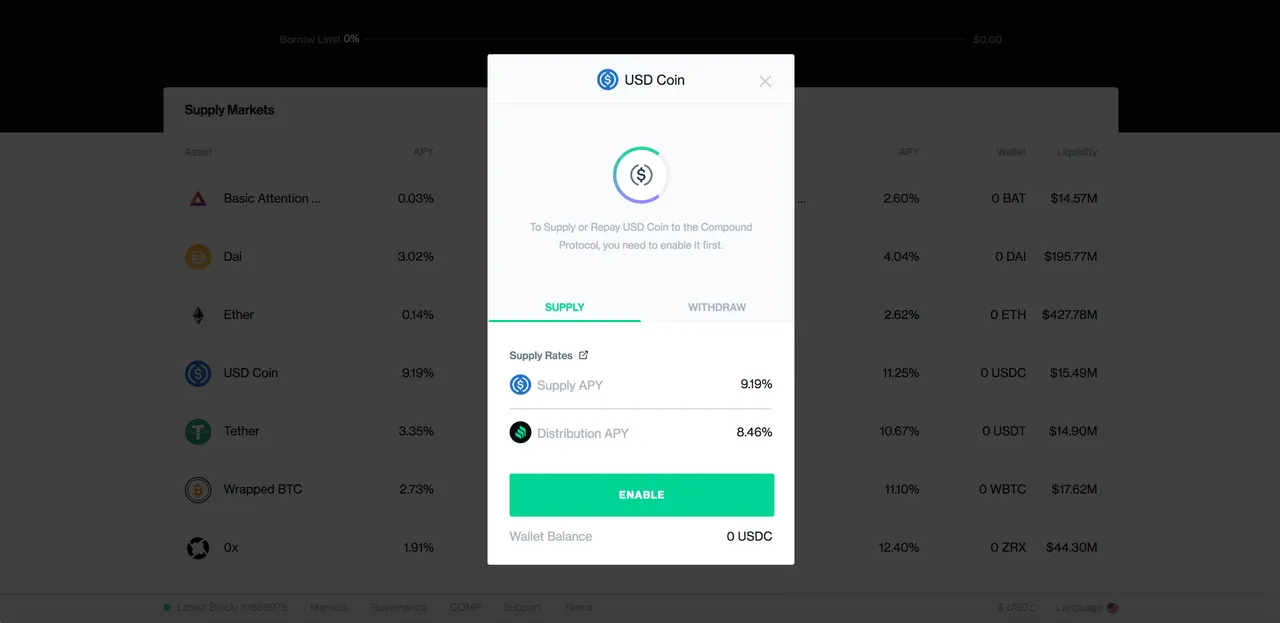

So for some cases, it's better than my Volksbank account. At least it doesn't say "Oh you cannot open your account as you said you cannot speak German". It happened to me 6-7 years ago even it's not written anywhere in there terms and conditions ... Of course I have to pay ETH to move crypto, gas fee to run Compound smartcontracts, and take risks of crypto such as volatility, hacking, managing things by myself etc.

Compound makes sense especially for rich people. If I have $1M, 10% APY for USDC means $10K. It's better than my estimated Japanese pension money ... 😂And the transaction/gas fee doesn't related to the amount of money. If I put my $1K ETH, it gives me few dollars. It'll vanish if the gas fee sky rockets ...

That's my understanding about Compound. Now I know why people are talking about it.

By reading DeFi and taking a look at services, now I slowly get to know the idea of "DeFi", "Yield Farming" ... etc.

I wasn't much interested in FinTech other than crypto and blockchain but DeFi is an interesting field :) I'm quite excited about it probably because it makes financial service really for everyone who are happy to learn (not just because of language, nationality) and also gives chance for us to design financial product by ourselves not by banks.

My mother told me my grandma was so happy with her first bank account and bank card. Financial services will change dramatically when my daughter grows up. I may talk about my crypto excitements to her as a good old time story 😁

先月末か今月の初めにDeFiについて @kinakomochi さんの投稿で読んで、興味が尽きずこの2週間くらいDeFiに関する文書や記事を読み漁っています。ようやくDeFiの概要がつかめてきて、昨晩は深夜までCompoundをのぞいて、エクセルで複利計算をして、感心していました。Compoundとは今回のDeFiバブルを牽引したプロトコルおよびそのプロトコルを使ったサービスです。

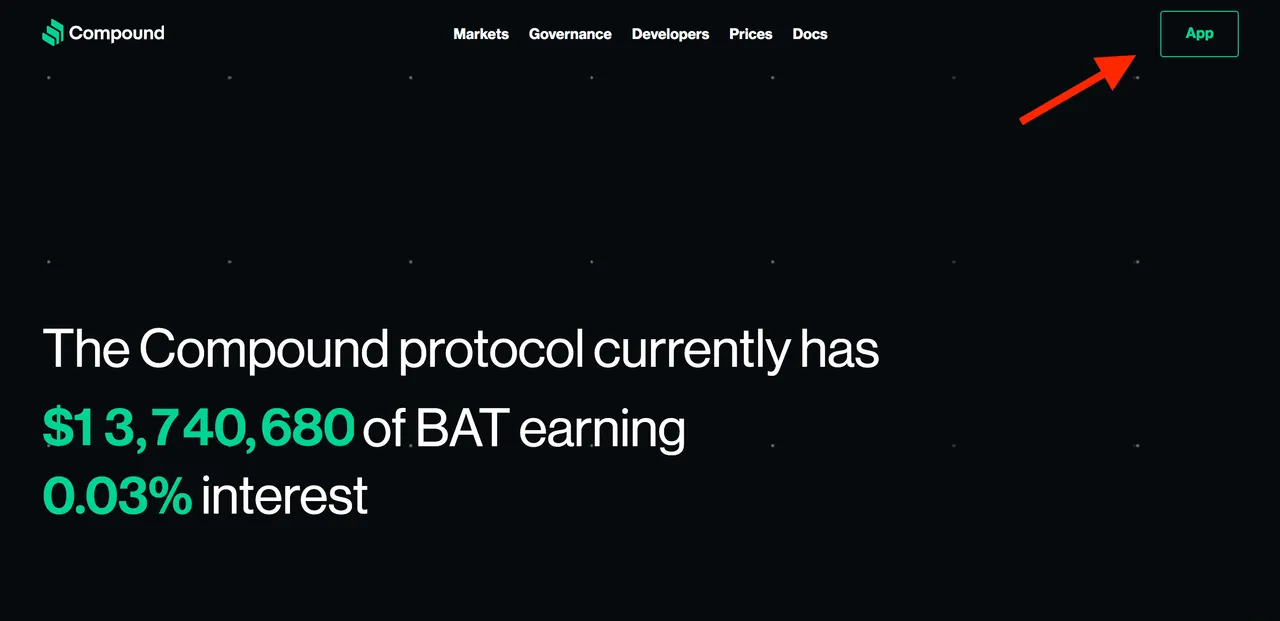

Compoundのウェブサイトをのぞいてみると、利率やプロトコル、インターフェイスについて書かれていて「あれ??レンディングサービスってよく聞くけど?」とよくわからなくなる人もいると思います。私もなりました。右上の「App」をクリックすると、レンディングサービスのページが表示されます。

MetamaskやWalletLink、WalletConnectに対応したウォレットをつないで、仮想通貨の貸し借りができるようになります。少し話がそれますが、モバイルウォレットを分散型アプリにつなげるWalletLinkは便利ですね。ブラウザ版メタマスクの100倍くらいスムーズで感動しました。

APYはリアルタイムの利率のようなもので、私のドイツの銀行口座では最大1.57%利息がつくことを考えると、仮想通貨によっては利率は結構よいのではないでしょうか。ちなみに調べてみたら三菱UFJ銀行の普通預金の利率は0.001%でした😅

さらにこのリストに表示されたAPYに加えて、貸し手にも借り手にもCompoundトークンが付与されます。

USDコインのAPYは昨日の夜は合計で17%を超えていました。日本もバブル期には利率7%の定期預金があり、10年でおよそ2倍になっていた時期がありますが、この利率は例外中の例外で、さらに定期預金なので満期になるまで引き出せないという制約があり、ほかの金融商品の利率はもっとよかったでしょう。

Compoundの場合、刻一刻と利息が支払われます。現在USDCやTether、Daiといったステーブルコインが高いのは仮想通貨が強気で、多くの人がボラティリティーの高い通貨を持つことからこれらの供給が少なくAPYが高いと理解すればよいのかな。逆に仮想通貨が弱気のときには多くの人が価格下落リスクを避けて資金をステーブルコインに逃避して、ボラティリティーの高い仮想通貨のAPYが高くなるのかな?これはあくまで私の推測です。

仮想通貨によっては銀行預金よりもいいですよね。もちろん送金手数料、ガス代、自己責任のリスクはつきまとうので、好みにもよりますが。あと、個人的に魅力を感じているのは、モバイルデバイスがあって、仮想通貨を持っていて、DeFiについて学ぶ意欲があれば誰でも使えるところだと思います。私はドイツに移住してすぐの頃に「ドイツ語話せないっていいましたよね、では当行では口座を開設できません」といったことがあったので(規約には全然そんなことは書いてなくて、法律を勉強していたパートナーが戦ってくれて無事口座を作れました)。

とはいえ、お金持ち向けのサービスといった感は否めません。というのももし私が1億円持っていたら、APY10%のトークンを貸し出して、年間100万円もらえます(複利は無視して単純計算)。これって私がもらえるであろう日本の国民年金より多い wwwwwwwww しかも送金手数料やガス代は金額に比例しないので、これらの手数料は無視できます。ステーブルコインを利用すれば価格変動リスクも小さくできます。一方、私が今Ethereumを10万円貸し出したとしても、年間数百円😂銀行の利率よりはましですが、働いた方がはやいです。

以上が私のCompoundに対する雑感です。富豪向けサービスとは思いつつ、CompoudはじめDeFiから見える未来にわくわくしています。フィンテックに対しては、ブロックチェーンと仮想通貨以外では、既存のサービスがデジタル化されただけで、そこまで興奮しませんでしたが、DeFiは何か違う気がします。本当に学ぶ意欲さえあれば国籍や居住地に限らず誰でも金融サービスが使えて、しかも銀行のような中央集権的な存在にサービスを与えられ搾取されるだけでなく作れるかもしれない。そんなところにわくわくするのだと思います。

母曰く、私の祖母は大喜びで初めてのキャッシュカードを手にしたといいます。子どもが大きくなる頃の金融サービスって大きく変わるんだろうな。