[ENG]

Big Blue balast-free

It took a while, but now it's finally gone, the tiresome and low-margin service business. A few weeks ago, a spin-off planned since 2020 was carried out and the subdivision was floated on the stock market as an independent company "Kyndryl". For years, this division had been dragging down the overall group in terms of growth and attractiveness from an investor's point of view. The stock market price is a long way from its former high of a good $200. Only the dividend has been raised further and further, and the dividend yield was recently a good 4% due to the decline in the share price. That is massive for a technology company. Apple or Microsoft, for example, are below 1%. But even that couldn't stop Warren Buffett, for example, from completely selling his position in IBM in 2018. From a previous perspective, completely rightly. The former stock market star and traditional company has fallen far behind.

Now IBM has the chance to focus on its prestigious, high-growth business areas of cloud computing, artificial intelligence and quantum computing. Hybrid cloud in particular is enjoying strong demand, and the AI "Watson" also promises more and more areas of application. In addition, IBM has a broad customer base cultivated over many years and still has a good reputation from PC times, when "IBM-compatible" was still a real trademark.

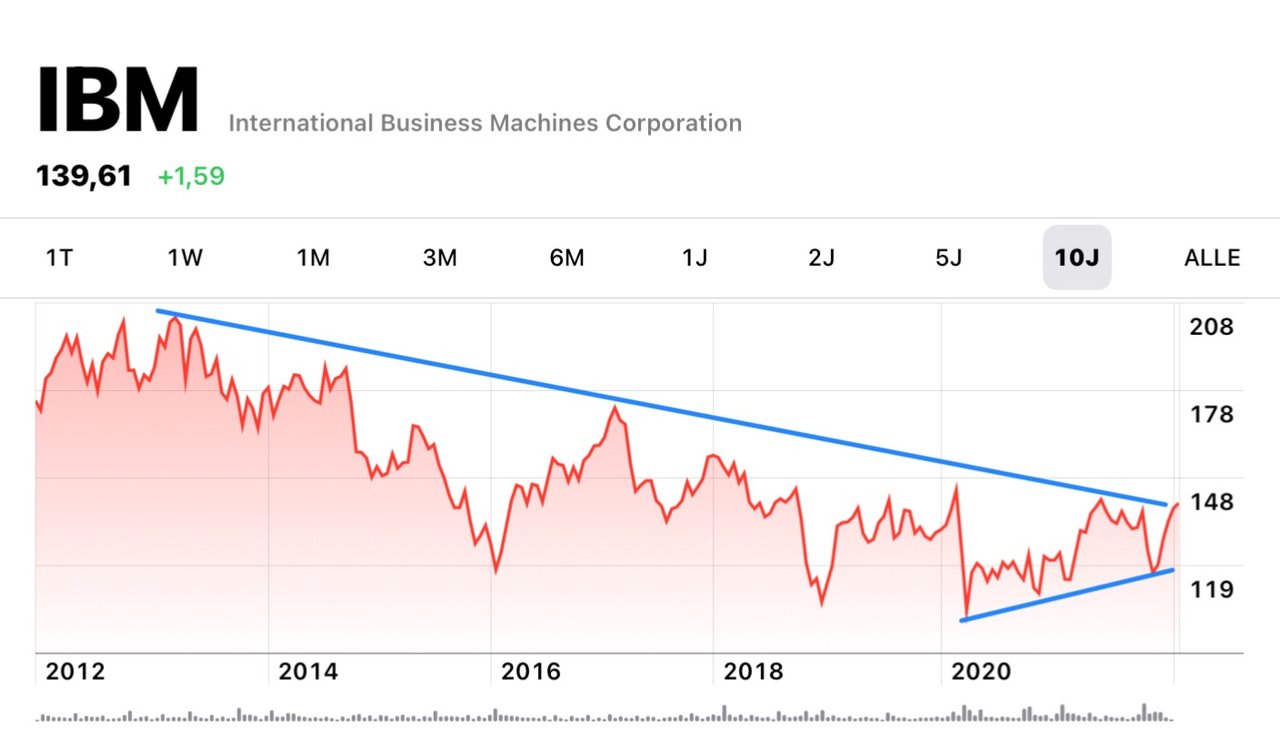

Downward trend before the break

If you look at the long-term price trend, you can see that we have now reached a very exciting point: The downtrend that has been in place since 2013 could be broken if we sustainably break above the resistance area at $140-145. Since the Corona Crash, we have been running upwards and the fundamental situation is promising as described above. The P/E ratio is moderate at 26. Microsoft or Apple are much more "expensive".

What do you think of the Big Blue? Do you think they will manage the turnaround?

—————

[GER]

Big Blue balastfrei

Es hat etwas gedauert aber nun ist man es endlich los, das leidige und margenschwache Dienstleistungsgeschäft. Vor einigen Wochen wurde ein seit 2020 geplanter Spin off durchgeführt und der Teilbereich als eigenständiges Unternehmen „Kyndryl“ an die Börse gebracht. Seit Jahren zog dieser Bereich den Gesamtkonzern runter, was Wachstum und Attraktivität aus Sicht der Investoren angeht. Der Börsenkurs ist weit vom einstigen Hoch von gut 200 $ entfernt. Lediglich die Dividende wurde immer weiter angehoben, die Dividendenrendite betrug wegen des Kursverfalls zuletzt gut 4%. Das ist massiv für einen Technologiekonzern. Apple oder Microsoft liegen zB. unter 1%. Aber auch das konnte beispielsweise Warren Buffett 2018 nicht davon abhalten, seine Position an IBM komplett zu verkaufen. Aus bisheriger Sicht völlig zurecht. Der frühere Börsenstar und Traditionskonzern ist weit zurückgefallen.

Nun hat IBM die Chance, sich auf seine prestigeträchtigen, wachstumsstarken Geschäftsbereiche Cloud Computing, Künstliche Intelligenz und Quantencomputer zu konzentrieren. Gerade die Hybrid Cloud erfreut sich starker Nachfrage und auch die KI „Watson“ verspricht immer mehr Anwendungsbereiche. Dazu hat IBM eine langjährig gepflegte breite Kundenbasis und ein immer noch gutes Renommee aus PC-Zeiten, als „IBM-kompatibel“ noch ein echtes Markenzeichen war.

Abwärtstrend vor dem Bruch

Schaut man sich den langfristigen Kursverlauf an, so erkennt man, dass wir mittlerweile an einem sehr spannenden Punkte angekommen sind: Der seit 2013 währende Abwärtstrend könnte gebrochen werden, wenn wir den Widerstandsbereich bei 140-145 $ nachhaltig überschreiten. Seit dem Corona Crash laufen wir nach oben und die fundamentale Lage ist wie oben beschrieben aussichtsreich. Das KGV ist mit 26 moderat. Microsoft oder Apple sind da deutlich „teurer“.

Was haltet ihr von the Big Blue? Glaubt ihr die schaffen den Turnaround?