Maker and DAI have been one of the crypto OGs. The idea behind the decentralized DAI stablecoin and its implementation have been extremely useful for some users. A very complicatied and innovative mechanics were put in places to achieve the DAI stablecoin. The protocol was on the top list for the TVL and the value it had accumulated.

Hoevere since last year the protocol rebranded to SKY and USDS, with a totally different way for minting USDS. As far as I’m aware and to my best knowledge, the new stablecoin USDS is no longer minted by putting collateral as ETH or BTC, but it is minted in a very similar way as the centralized stablecoins USDT and USDC. That is by putting USD in a bank or buying short term treasuries bonds. There is the new governance token on top of it SKY, that probably serve some purpose and is being rewarded also as a yield.

It’s a completely different setup that what the old version was, and I must put my speculation here that this is in favor of the dollar, to avoid a popular options for creating synthetic dollars, but to push the demand for dollars towards USD debt and bonds.

The old version of DAI and MAKER are still around and they work but they are slowly being decommissioned and converted to the new version via an upgrade function.

More to read on MakerDAO in there whitepaper on the link.

Here we will be looking at:

- Total value locked TVL (collateral)

- DAI supply

- Loan to value ratio LTV

- Top tokens used as collateral

- Defi protocols rank by TVL

- Number of users DAUs

- Price

The period that we will be looking at is 2020 - 2024.

The data here is compiled from different sources like DefiLama and Dune Analytics.

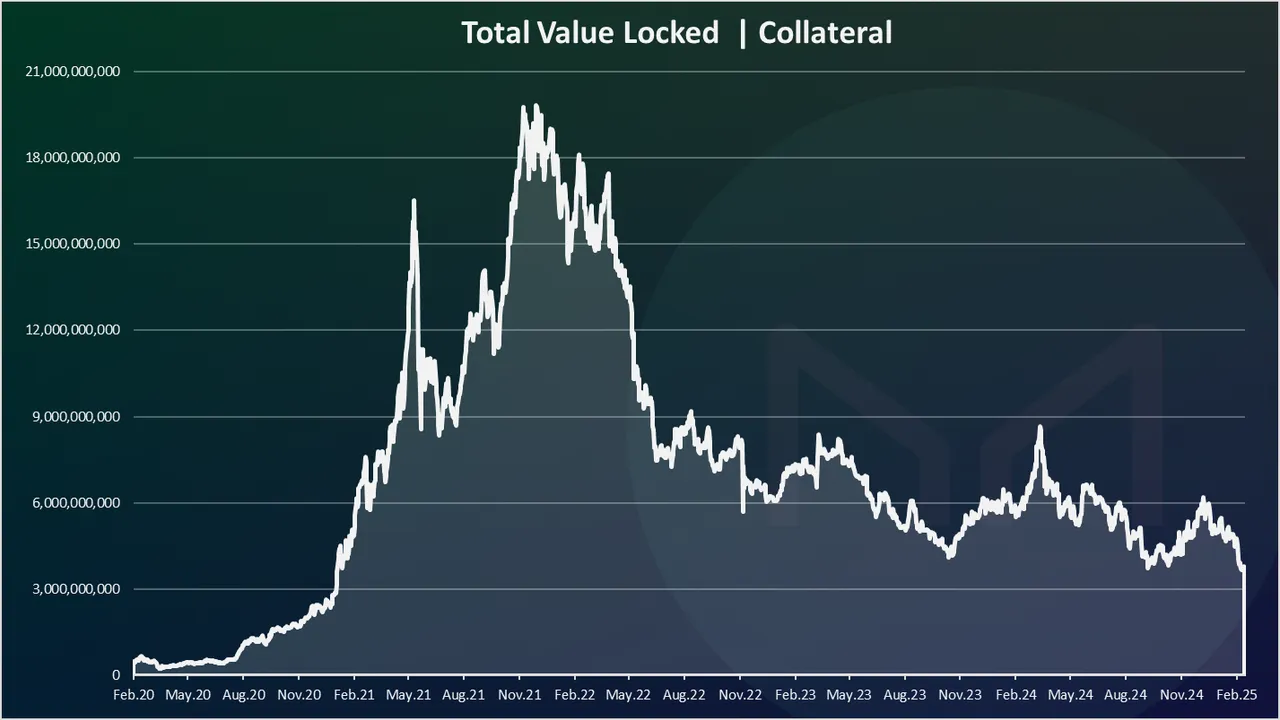

Total Value Locked | Collateral

In the case of MakerDAO the TVL is the collateral deposited to mint DAI. Here is the chart.

The TVL for MakerDAO was quite small back in 2020. It was under 100M. Then it started growing and in 2021 it has grown exponentially. The ATH for the collateral value in the MakerDAO protocol was reached at the end of 2021 with almost 20B in value.

The 20B was the ATH for Maker, as it never recovered back to those highs and with the latest happenings and transition to SKY/USDS it will never be at that point again. At the moment the TVL is at 3.7B.

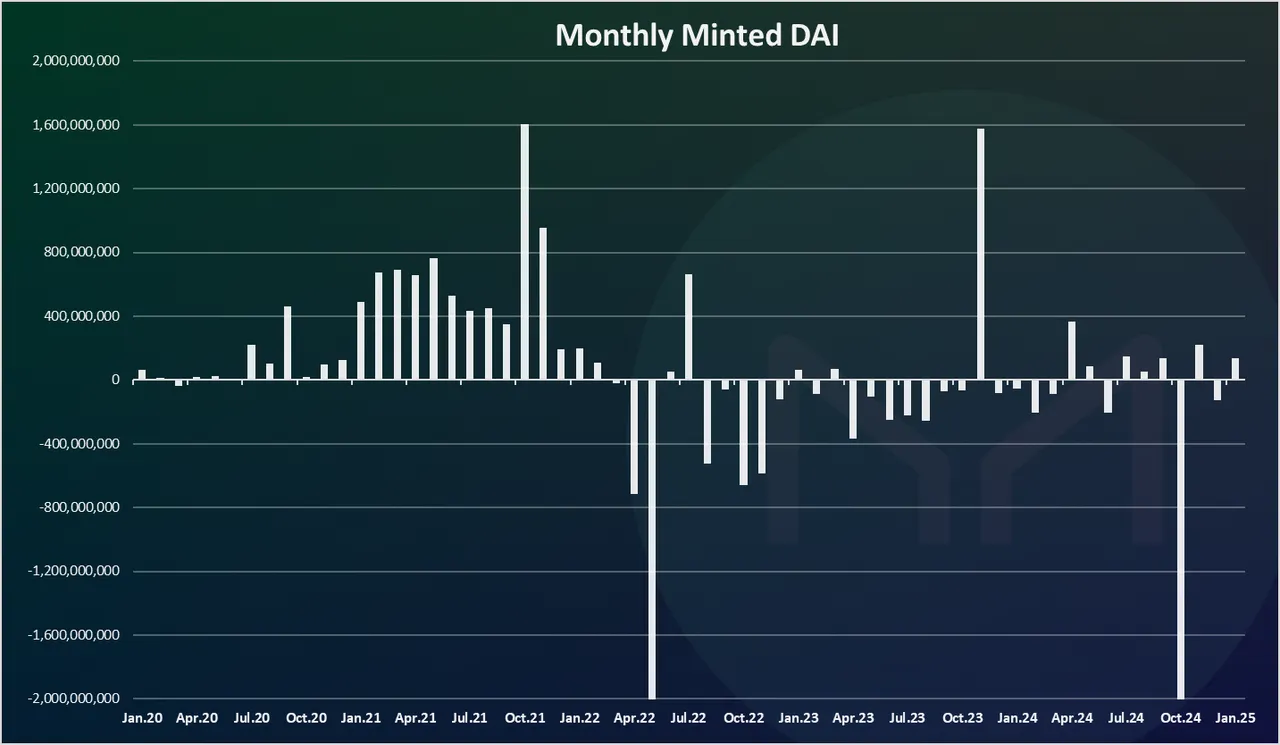

DAI Supply

Here is the chart for DAI minted per month.

Here we can see the constant positive months back in 2021 with around 700M DAI minted on a monthly basis, and a record of 1.6B in October 2021.

In May 2022 there was a negative 2.2B DAI burnt.

In 2023 we can notice the big spike in November, when 1.5B new DAI was minted. The other months are with a lot less volatility.

We can notice the sharp drop in October when more than 2B DAI was burned, and I’m guessing a lot of it was converted to the new version USDS.

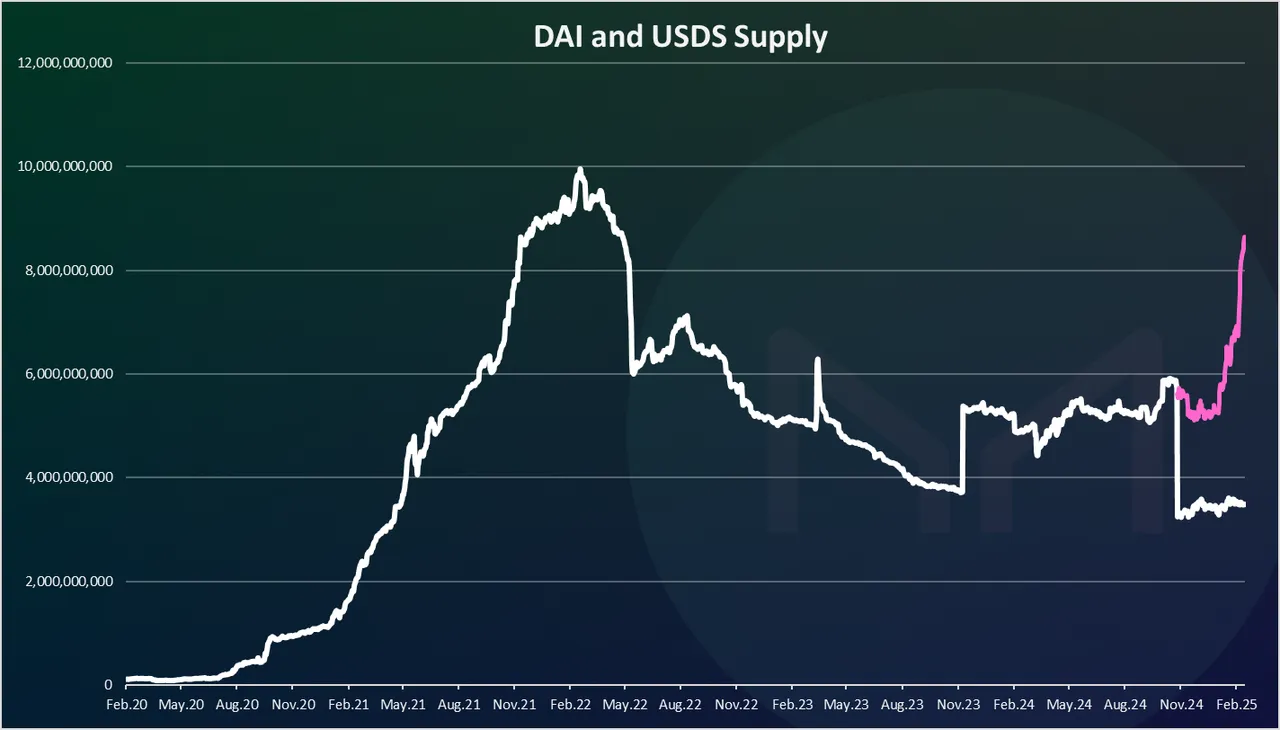

The cumulative DAI and USDS in circulation chart looks like this:

I have added the USDS supply to this chart for context. The chart is not staked, meaning it gives the value for each coin, not the cumulative.

As we can see, in October last year there was a drop in the DAI supply, while USDS started at 5B. It has grown fast since then and it is now at 8B, while DAI is at 3.4B.

The DAI supply has grown massively in 2021 and the first half of 2022, reaching an ATH of 10B. Then UST happened, the stablecoin marketcap dropped a lot in May 2022, and has continued to go down ever since. A short spike in March 2023, due to the USDC situation. Another spike in November 2023 and almost constant with even a slow decrease in the last months with around 5B DAI in circulation.

It’s interesting to see that with the increase of the crypto prices the amount of DAI in circulation has stayed relatively same. DAI has shown that is resilient and survived bear market, but its grow has been somewhat stale.

Loan to Value Ratio LTV

The LTV value is often used for MakerDAO and DAI, to access the overall health of the ecosystem and the collateral position. It is a ratio between the value of the collateral deposited and the DAI minted. For example, for a 10B in collateral and 5B DAI minted the LTV ratio is 10/5 = 2, or 200% percent. Here is the historical chart.

From the chart above we can notice that the LTV value has dropped over time. At the beginning of 2020 this ratio was at 500%, while in the last year it is around 150% or less.

While this ratio might seem low and might show that there are a lot of vaults close to liquidation, we should bear in mind the type of collateral that is being used over time. At first ETH was the number one collateral and was dominant. But as time progressed USDC became a large share of the collateral to mint DAI. Since USDC is pegged to the dollar there is no need for overcollateralization like in the case of ETH and users are minting DAI for 1 to 1 ratio. This lowers the overall LTV ratio.

In the last period the collateral structure for minting DAI has changed and migrated back from USDC to mostly Ethereum. Because of this we can see a recent spike in the LTV ratio.

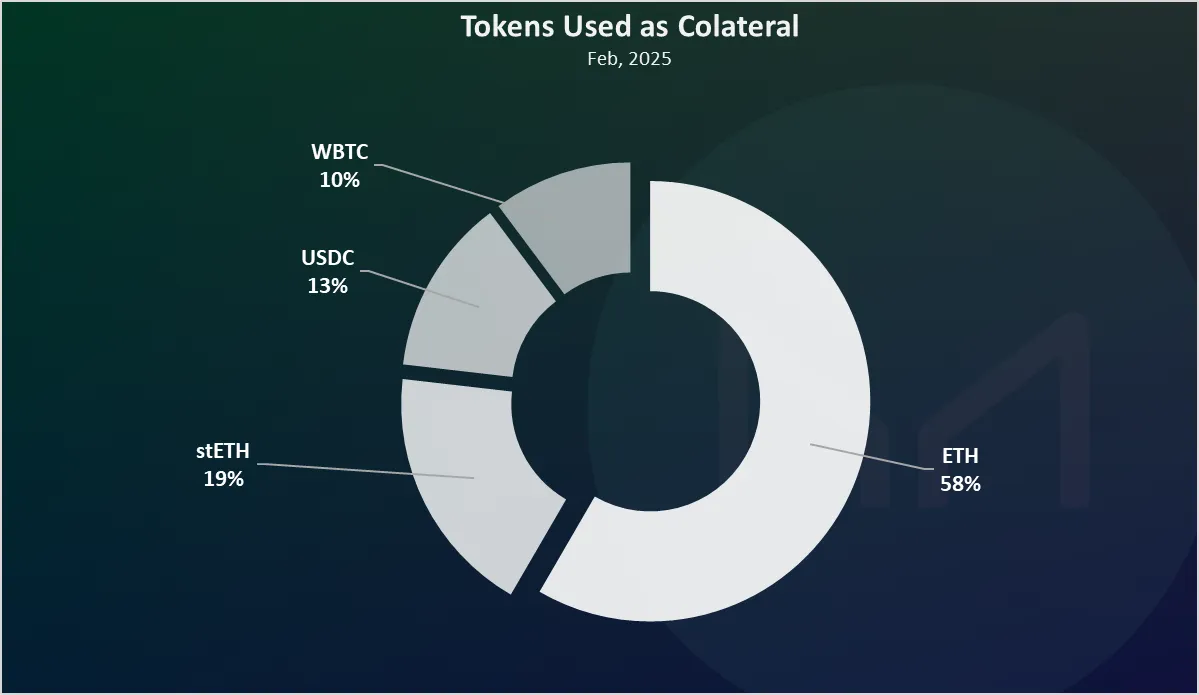

Top Tokens Used as Collateral

Which tokens are used the most when minting DAI. Here is the chart.

This is an old chart for the allocation as I wasn’t able to find an up to date data. Back in August ETH and it staked version stETH were the dominant way how DAI was minted. This is now probably losing relevance, as not a lot of new DAI is being minted by catheterization and the new mints are forwarded towards USDS, meaning now the dominant way for minting is US debt.

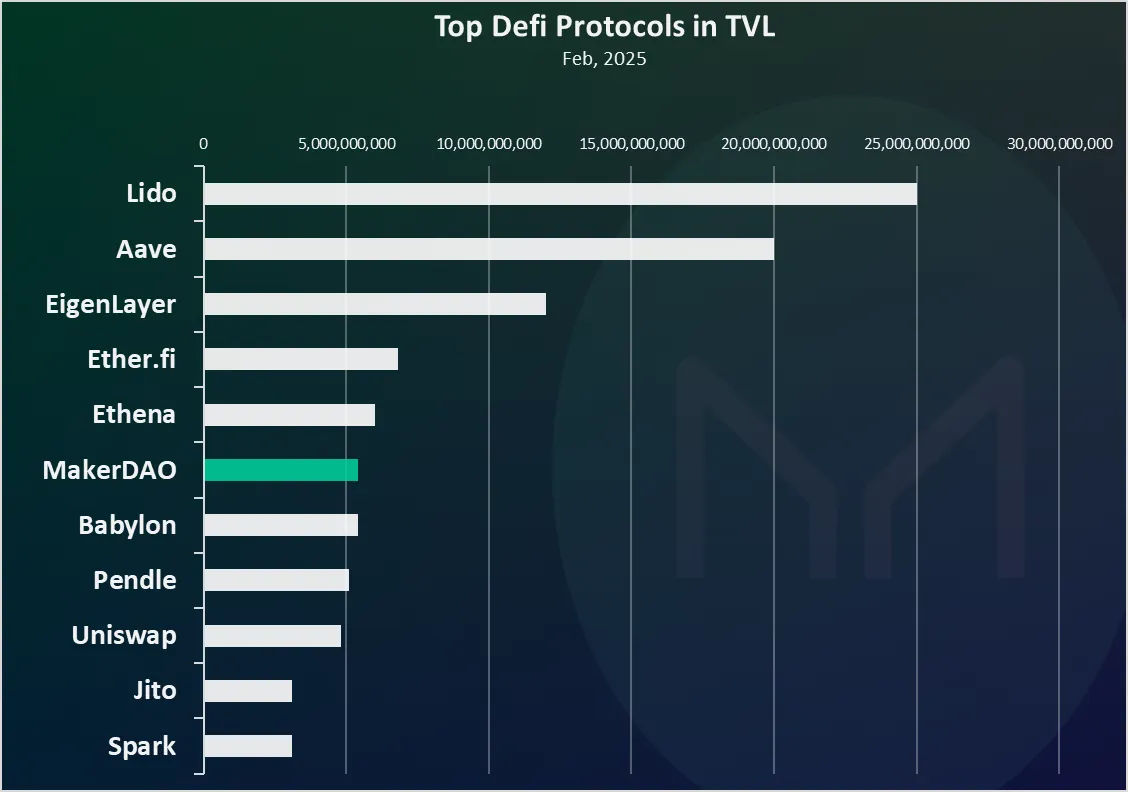

Top Defi Protocols Ranked by TVL

How is the MakerDAO protocol doing when compared to the other ones? The total value locked is usually one of the metrics these protocols use.

Here is the chart.

MakerDAO is now in the middle of the chart. Back in the days it was number one for a long time. It has obviously stepped down, and my guess is that it was forced to. This just show how important is the stablecoin sector.

Price

When it comes to prices, we will be looking at the chart for the governance token MAKER and the stabelcoin DAI.

Here is the chart for the MAKER token.

Quite a wild ride for MAKER, going from 400 to more than 5k in 2021, and down to 600 in 2022.

There was sharp growth again in the first half of 2024 and a drop afterwards, especially during the transition period in October 2024. It is now trading around 1k and is close to the previous lows.

Maker has transitioned and started buying US debt as a clolateral for a stablecoin, totaly going out of the initial idea of decentralized stablecoin. It is all confusing now, how it works and what aspect of it are actualy decentralized. I'm not sure what is the new role of the new governance token SKY. To bad it is ending this way. At least we have HBD on HIVE!

All the best

@dalz