Index - https://steemit.com/tax/@alhofmeister/3fyvxh-tax-blog-index

Introduction

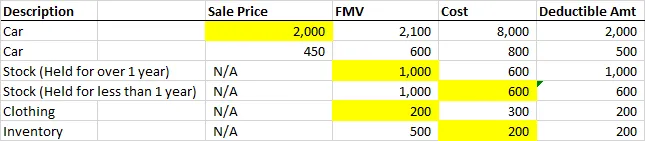

The purpose of this posting is to further demonstrate the effect of the charitable contribution deduction. This example looks at contribution of 6 different types of items and the amount that would be deductible (before applying the AGI limitations explored earlier). For the 2 cars, the charitable organization immediately sold the property after contribution. The sales proceeds from the cars are listed under "Sale Price". Additionally, both cars were held for over a year.

Solution

The deductible amount for the first car would be the sale price by the charitable organization as it is less than the fair market value of the vehicle upon contribution. Since the 2nd car was sold for less than $500, the deductible amount would be the lesser of $500 or it's fair market value. The stock held for more than 1 year would qualify as long-term capital gain property, and would be deductible at it's fair market value as a result. The stock held for less than 1 year would be deductible at it's fair market value less any ordinary gain associated with the property ($400 in this case since the stock originally cost $600). The clothing would be deductible at it's fair market value of $200 whereas the inventory would be subject to a similar treatment as the stock held for less than a year (unless it is food).

References

https://steemit.com/tax/@alhofmeister/charitable-contributions

Disclaimer

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.